Interest Rate & Market Commentary for Week Ending 15th August 2025

Weekly Overview

The S&P 500 and the NASDAQ climbed around 1%, recording their second positive week in a row but failing to match the previous week’s stronger gains. It was the sixth positive week out of the past eight for both indexes.

The Dow climbed 1.7% for the week but finished 0.2% shy of joining the S&P 500 and the NASDAQ in record territory. While the Dow has yet to breach the historic peak that it reached last December, the other two indexes have remained above their late 2024 peaks for the past seven weeks, pushing their records higher

A U.S. small-cap stock benchmark rallied to gains of 3.0% and 2.0%, respectively, on Tuesday and Wednesday en route to an overall weekly result that outperformed a large-cap index by a wide margin. The small-cap benchmark finished 3.1% higher for the week versus a 1.0% gain for its large-cap counterpart.

The most widely traded cryptocurrency rose modestly for the week overall after briefly surging to a record high. The price of Bitcoin topped the $124,000 level on Thursday, but it fell back to around $118,000 later in the day and was trading around $117,000 on Friday afternoon. On a year-to-date basis, Bitcoin was up nearly 26%.

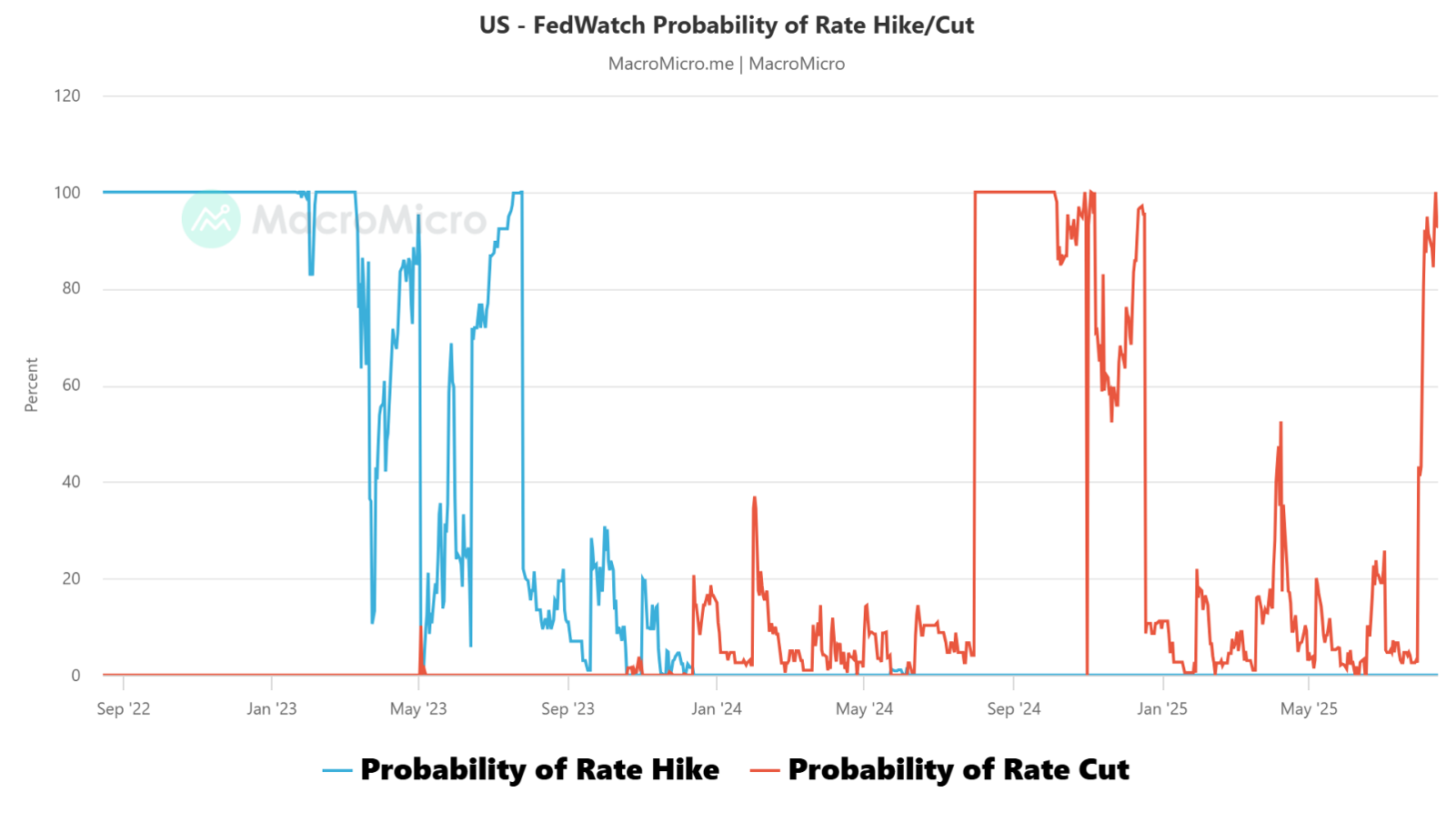

Bond market trading on Friday continued to support recently growing expectations that the U.S. Federal Reserve is likely to cut its benchmark interest rate at its two-day meeting ending September 17. Prices in rate futures markets implied that most investors were expecting this year’s first quarter-point rate cut at next month’s meeting, with the prospect of one or two further cuts in October and December, according to CME Group’s FedWatch tool.

Investors and economists will turn their attention to the Rocky Mountain town of Jackson Hole, Wyoming, where the U.S. Federal Reserve will hold its annual three-day economic policy symposium beginning Thursday, August 21. Fed Chair Jerome Powell is among the featured speakers, with an address scheduled on Friday.

Two reports presented a mixed picture of elevated inflationary pressures at the consumer and wholesale levels. The Consumer Price Index showed that inflation held steady at a 2.7% annual rate in July, even as higher tariffs appeared to boost prices at faster rates for some categories of goods. While that consumer report was in line with expectations, producer prices reflecting business costs recorded a bigger-than-expected 3.3% increase—the sharpest rise in five months.

U.S. retailers recorded a 0.5% month-over-month sales gain in July, matching economists’ consensus forecast but trailing the prior month’s upwardly revised figure of 0.9%. A separate report on Friday showed a weakening of U.S. consumer sentiment for the first time in four months and an increase in consumers’ inflation expectations.

Trump Tariffs – Chips and India

India’s 50% tariff targets energy trade imbalances, with 35.8% of crude imports from Russia versus 3.5% from the U.S., while exempting refined oil, pharmaceuticals, and consumer electronics, protecting nearly 16% of U.S. exports and supporting Apple’s supply chain as India became the top U.S. mobile phone supplier in April-May 2024. Limited U.S. trade exposure (4.3% of GDP) gives India negotiating resilience compared to Vietnam and Thailand. The Reserve Bank of India’s rate stability preserves monetary flexibility, while the selective exemptions allow India to maintain export revenue, apply pressure on secondary sectors, and incentivize energy trade rebalancing without triggering widespread economic disruption.

Even though Trump left some wiggle room to strike a deal, his vitriolic comments about India are upending a decades-long push by the US to court the world’s most populous country as a counterweight to China.

On August 7, Trump announced sweeping 100% tariffs on semiconductor imports, paired with exemptions for firms investing in U.S. manufacturing. Apple pledged an additional $100 billion, while Taiwan’s TSMC, Wistron, Yageo, and Pegatron also qualified through U.S. facility commitments.

Companies showing intent without progress risk audits and back-tax liabilities, creating strong pressure for tangible deployment. In parallel, unprecedented revenue-sharing deals now require Nvidia and AMD to remit 15% of China-related chip sales to the U.S. government as export license conditions, potentially generating $1 billion per quarter from Nvidia’s H20 sales alone. Nvidia CEO Jensen Huang’s White House meeting paved the way for this landmark arrangement, marking the first time firms must pay revenue percentages for trade privileges. The announcement coincided with India doubling chip tariffs to 50% and the August 12 China trade deadline, signalling coordinated global pressure tactics designed to reshape semiconductor supply chains and strengthen U.S. leverage in negotiations.

Despite massive investment pledges, U.S. semiconductor capacity remains highly constrained, with TSMC’s expanded operations lifting domestic share from just 6% to 11% of global output. Even with Apple’s $600 billion and TSMC’s $100 billion commitments, self-sufficiency is decades away. Current production covers less than 12% of U.S. demand, and CHIPS Act projections fall short of closing the gap. Severe talent shortages, up to 77,000 engineers and 69,000 technicians, further limit progress. Trump’s 100% tariff threat thus functions mainly as negotiation leverage, consistent with his past tactics. Exemptions for firms investing in U.S. capacity, coupled with Nvidia/AMD revenue-sharing, emphasize financial extraction over true reshoring.

Chinese chipmakers have little U.S. market presence, making Trump’s 100% tariff threat more about extracting concessions from non-Chinese firms ahead of U.S.-China trade talks. The 15% revenue-sharing deal on Nvidia and AMD’s China sales channels funds directly to Washington, with Nvidia’s H20 chips alone potentially generating $1 billion quarterly. This arrangement balances economic benefit with controlled Chinese AI access, limiting tech transfer without full prohibition. Beijing’s criticism of H20 reflects concern over U.S. leverage. Trump’s reversal of the H20 ban after Nvidia’s White House meeting underscores tactical flexibility, preserving U.S. gains while keeping semiconductor ties as bargaining leverage.

The semiconductor tariff framework’s success hinges on sustaining negotiation pressure without disrupting U.S. technology leadership or alliances. Revenue-sharing deals risk undermining national security rationales and allied cooperation, complicating future multilateral tech restrictions. Key focus areas include August 15 U.S.-Russia talks and India’s potential engagement with China, which could affect Asia-Pacific strategic alignment. Market attention on Modi’s first China visit in seven years underscores tensions between economic leverage and alliance goals, especially amid the U.S.-India trade expansion target of $500 billion by 2030. The policy’s effectiveness relies on selective technology access to balance revenue generation with maintaining strategic tech control.

US GDP Momentum – Soft landing expected

The 3.0% annualised rebound in Q2 GDP is largely misleading, as it stems almost entirely from tariff-driven trade distortions rather than genuine domestic strength. Imports collapsed by -30.3%, reversing Q1’s +37.9% surge, as businesses unwound earlier tariff-related stockpiling. This sharp drop narrowed the goods trade deficit to $86 billion, back to 2023 levels, but the improvement reflects inventory adjustments rather than a healthier economy. Stripped of this volatility, core private sector momentum shows clear weakness.

Final sales to private domestic purchasers, consumption plus private investment excluding government and trade, slowed to just 1.2% annualized growth, down from 1.9% in Q1. This marks the weakest pace since 2022 and highlights a significant deceleration in underlying activity. In short, the headline GDP figure overstates economic resilience, as the underlying trend points to weakening private demand and investment momentum masked by temporary trade distortions.

Consumer spending showed only modest improvement in Q2, with goods rising 2.2% annualised and services 1.1%. However, both remain well below prior-year levels, and services, the largest share of the economy, expanded just 1.9% year-over-year, slipping beneath the 2% threshold. This slowdown is troubling because services usually provide stability during manufacturing downturns, suggesting weakness is now spreading across the broader economy. The concurrent softening in both goods and services indicates a demand-driven slowdown rather than a temporary, tariff-related supply disruption. Evidence from the San Francisco Fed supports this view, showing tariffs may temporarily support manufacturing but ultimately reduce consumer purchasing power, cooling services demand. For a services-dominated economy like the U.S., this dynamic has a net negative effect. Overall, the data signals a genuine deceleration in consumer activity, highlighting diminished underlying momentum rather than a short-lived adjustment to trade distortions.

The labor market reflects a fragile “three-low” equilibrium, low supply, low hiring, and low layoffs. Labor force participation has slipped to 62.2%, the lowest since 2022, while unemployment rose modestly to 4.2% as workforce contraction offsets weaker demand. Unlike typical recessions with mass layoffs, this gradual cooling suggests a slowdown that policy can manage. Governor Bowman notes firms remain reluctant to cut staff, recalling pandemic shortages, which helps buffer recession risks. Employment weakness is broad-based, but education and healthcare largely sustain payrolls. Overall, the data points to a managed slowdown rather than imminent collapse.

The difference between a managed slowdown and a pre-recession stall lies in timing of policy support. With the Fed set to begin cutting rates in September, monetary easing arrives before fragile labour conditions translate into mass layoffs. This proactive stance contrasts with past cycles where delayed action deepened downturns. Historical patterns show tariff-driven slowdowns can achieve soft landings if paired with accommodation. The current 125bps easing cycle offers far more support than the restrictive 2018 backdrop. Combined with gradual demand cooling, worker hoarding by businesses, and broad policy responsiveness, the base case remains a slowdown—not a slide into recession.

Market Summary Table Week 15th August 2025

| Name | Week Close | Week Change | Week High | Week Low |

|---|---|---|---|---|

| Cash Rate% | 3.60% | |||

| 3m BBSW % | 3.612 | -0.0786 | 3.612 | 3.612 |

| Aust 3y Bond %* | 3.325 | -0.052 | 3.377 | 3.322 |

| Aust 10y Bond %* | 4.23 | -0.026 | 4.257 | 4.215 |

| Aust 30y Bond %* | 4.97 | -0.006 | 4.976 | 4.946 |

| US 2y Bond % | 3.7233 | -0.016 | 3.754 | 3.687 |

| US 10y Bond % | 4.281 | 0.0271 | 4.293 | 4.24 |

| US 30y Bond % | 4.8725 | 0.0432 | 4.885 | 4.828 |

| iTraxx | 67 | 0 | 71 | 67 |

| $1AUD/US¢ | 65.1 | -0.100 | 66.01 | 59.54 |

Chart of the week: Probability of Fed Rate Cut

The base case scenario of “economic slowdown enabling Fed rate cuts without falling into recession” remains intact, supported by businesses’ reluctance to lay off workers, gradual rather than sudden demand deceleration, and policy makers’ proactive rather than reactive stance on providing economic support. The current cash rate market expectations show the probability of a rate cut to be almost 100%. Last week’s equity and bond market price action has been driven by these expectations.

Overview of the US Equities Market

Wall Street traders sent stocks down from all-time highs as data showed mixed indications on how American consumers are feeling about the economy. Investors also kept a close eye on a face-to-face meeting between Donald Trump and Vladimir Putin.

The S&P 500 and the NASDAQ climbed around 1%, recording their second positive week in a row but failing to match the previous week’s stronger gains. It was the sixth positive week out of the past eight for both indexes. The Dow climbed 1.7% for the week but finished 0.2% shy of joining the S&P 500 and the NASDAQ in record territory. While the Dow has yet to breach the historic peak that it reached last December, the other two indexes have remained above their late 2024 peaks for the past seven weeks, pushing their records higher.

A U.S. small-cap stock benchmark rallied to gains of 3.0% and 2.0%, respectively, on Tuesday and Wednesday en route to an overall weekly result that outperformed a large-cap index by a wide margin. The small-cap benchmark finished 3.1% higher for the week versus a 1.0% gain for its large-cap counterpart. Trump greeted his Russian counterpart with a handshake in Alaska as they kicked off a highly anticipated summit, with the US leader looking to secure an end to the war in Ukraine. A joint press conference was planned for after their meeting.

Before that, economic data showed a broad-based advance in US retail sales, boosted by car sales and major online promotions. Later, a separate report showed consumer sentiment unexpectedly fell for the first time since April, and inflation expectations rose.

Markets are still wholly convinced that officials will cut rates by 25 basis points in September and follow that up with at least one other cut in October or December, noted Paul Ashworth at Capital Economics. He says Powell will possibly caution that a modestly restrictive policy stance remains appropriate. At Bank of America Corp., strategists led by Michael Hartnett say US stocks are set to decline in the event of dovish signals from the Fed in Jackson Hole as investors “buy rumor, sell fact.”

Investors poured about $21 billion into US equity funds in the week through Aug. 13, after redeeming nearly $28 billion in the week prior, according to a BofA note citing EPFR Global data. Retail investors are increasingly validated in the buy-the-dip approach, given the speed of the recovery from the recent selloff, potentially creating a self-fulfilling prophecy the next time the market experiences a minor selloff, according to Mark Hackett at Nationwide.

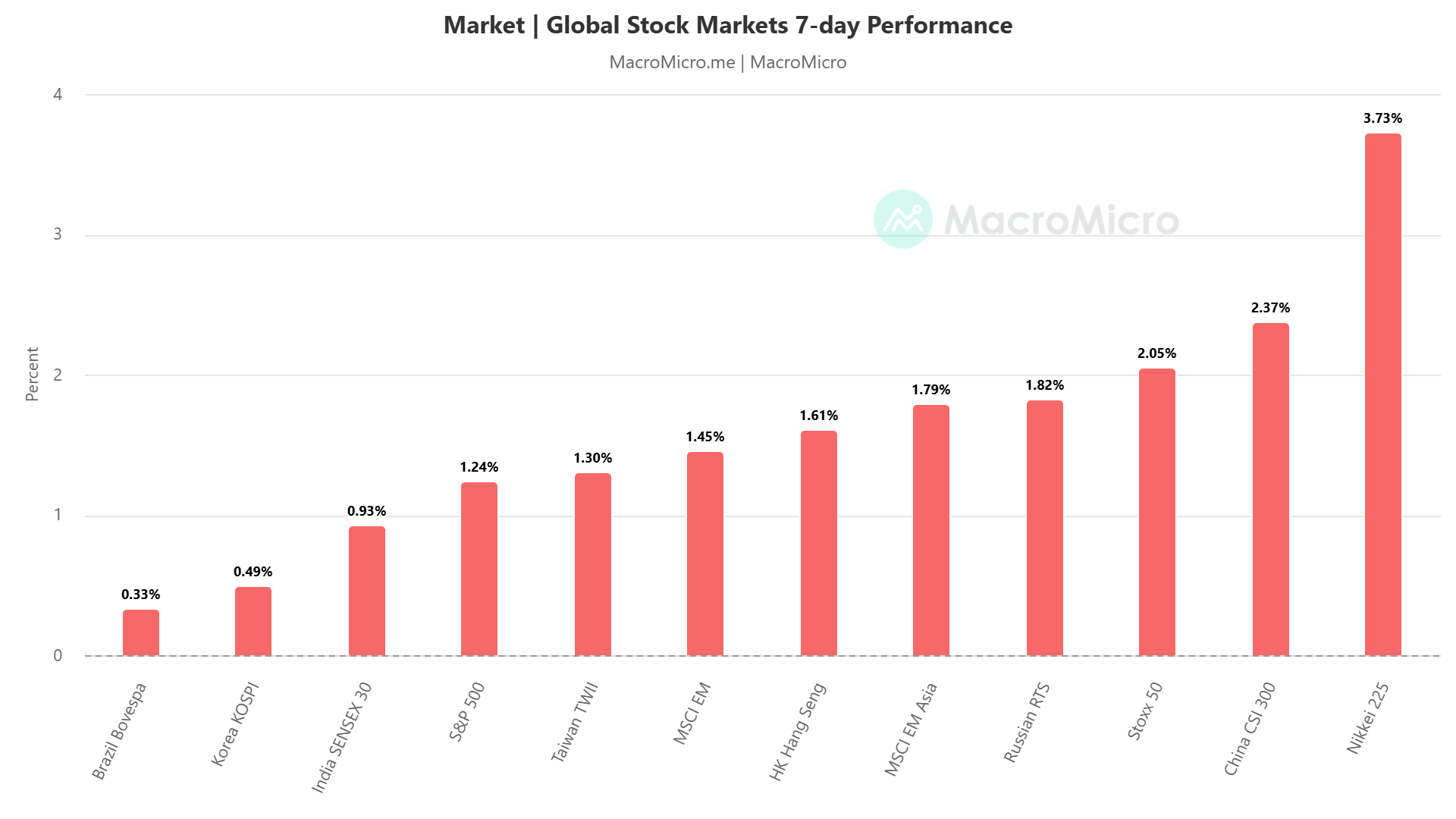

Over the past week, best stock market performance was noted in Japan (+3.7%) and China (+2.37%). EM beat DM and S&P500. Brazil, Korea and India all rallied but lagged the S&P500 performance.

Figure 1 – 7-day Performance of Global Stock Markets

Overview of the US Treasuries Market and Other Fixed Income Markets

Bond market trading on Friday continued to support recently growing expectations that the U.S. Federal Reserve is likely to cut its benchmark interest rate at its two-day meeting ending September 17. Prices in rate futures markets implied that most investors were expecting this year’s first quarter-point rate cut at next month’s meeting, with the prospect of one or two further cuts in October and December, according to CME Group’s FedWatch tool.

Trump nominated Stephen Miran to fill Kugler’s vacant Fed Board seat, adding a dovish voice aligned with pro-cut governors Waller and Bowman. Miran, a key Trump economic advisor and tariff policy architect, combines dovish leanings with experience using monetary policy to offset trade shocks, linking Trump’s agenda with Fed independence. Bloomberg reports Waller, who dissented in July for immediate cuts, is now Trump’s top Fed Chair pick, surpassing Warsh and Hassett. While Trump derides Powell as “Mr. Too Late,” Powell has already shifted dovish, stressing employment risks and setting up September cuts based on fundamentals, not political pressure.

The 2026 Fed voting rotation removes two of the most hawkish voices, Schmid (Kansas City) and Musalem (St. Louis) and brings in a more dovish set of regional presidents: Hammack (Cleveland), Logan (Dallas), Paulson (Philadelphia), and Kashkari (Minneapolis). Kashkari, who recently pushed for two cuts in the dot plot, underscores the shift toward a neutral-to-dovish bias, softening the committee’s stance even before any Trump-driven appointments take effect. At the same time, Waller’s emergence as Trump’s leading Fed Chair candidate offers strong political optics. His internal promotion would avoid credibility risks linked to outsider nominees like Warsh or Hassett, ensuring continuity, market stability, and alignment with Trump’s push for easier monetary policy while preserving institutional legitimacy.

The alignment of Stephen Miran’s dovish appointment, Waller’s likely elevation to Fed Chair, and the 2026 voting rotation sets the stage for a 125bps easing cycle, 75bps in H2 2025 and 50bps in 2026. This sequencing enables steady policy accommodation across political transitions, with Waller’s internal promotion ensuring continuity from his current dissenting role to potential chairmanship, avoiding disruptions typical of outsider appointments. Unlike Trump’s first term, when rate hikes clashed with trade war pressures, the upcoming cycle positions monetary policy as a stabilizer against tariff impacts while preserving Fed independence. The rotation’s built-in dovish tilt, coupled with Trump’s preference for pro-cut nominees, guarantees accommodative momentum without resorting to controversial removals, protecting institutional credibility and avoiding constitutional risks over central bank autonomy.

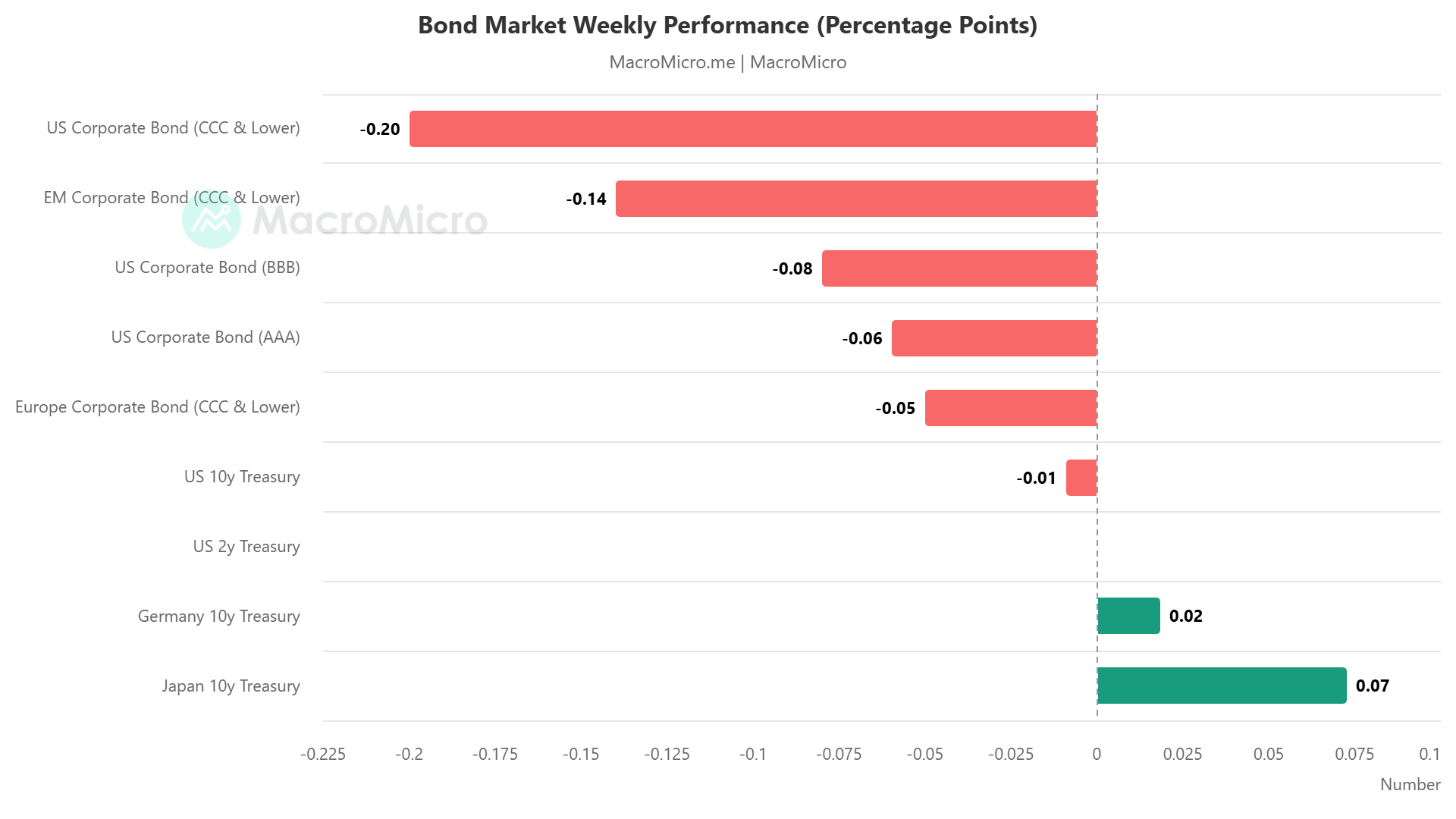

Figure 2: Bond Market Weekly Performance

Following the passage of the One Big Beautiful Bill Act (OBBBA), the US debt ceiling was raised by $5 trillion, bringing total federal debt to $36 trillion. This allows the Treasury to resume issuing debt after months of disruption.

According to updated Treasury estimates released on July 28, borrowing for the July–September quarter is now expected to reach $1.01 trillion—almost twice the $554 billion projected in April. The sharp increase is aimed at quickly restoring the Treasury General Account (TGA) to $850 billion. For the October–December period, the Treasury plans to borrow an additional $590 billion.

Heavy debt issuance after a debt ceiling increase isn’t new—we’ve seen this pattern many times. With a wave of supply coming in a short window, what does this mean for the bond market and equity market liquidity?

Overview of the Australian Equities Market

The Australian share market closed the week at record highs, with the S&P/ASX200 surging 64.8 points (0.73%) to 8,938.6 and the broader All Ordinaries rising 63 points (0.69%) to 9,212.1, marking its best-ever close. The week delivered a 1.4% gain for the ASX200, supported by easing worst-case tariff fears, an RBA interest rate cut, strong Wall Street performance, and positive local earnings. Nine of 11 sectors finished higher, led by financials, mining, and energy.

The big four banks all closed in the green, with Westpac up over 8% in two days and CBA recovering post-earnings. Major miners including BHP, Fortescue, and Rio Tinto rose over 1.1% amid hopes of Chinese stimulus. Energy shares outperformed, boosted by Ampol’s $1.1 billion acquisition of EG Group’s Australian assets, while Cochlear edged up 1% despite underwhelming profits. Gold miners benefited from a weaker Australian dollar, though Bitcoin fell over 4% after a recent record. The coming fortnight is set for high volatility as major companies like BHP, Woodside, Goodman Group, and CSL release results, while US-Russia talks in Alaska could add further market attention. The Aussie dollar ended slightly weaker at 65.07 US cents.

Reporting Season

The Australian company reporting season has begun in earnest, with investors closely watching earnings results that could set the tone for markets over the next two weeks. This period is particularly significant as it is the busiest fortnight of the year for corporate disclosures, with major companies across sectors releasing financial results. Key reporting names include BHP, Woodside, Goodman Group, CSL, Cochlear, and the big four banks, whose earnings and guidance are expected to influence broader market sentiment.

Early results have shown a mixed picture. Financials, including the major banks, have generally performed well, with Westpac rebounding strongly and CBA recovering after a post-earnings dip. Mining companies have benefitted from expectations of stimulus measures in China, lifting materials sector stocks. Energy companies, such as Ampol, have also attracted attention following strategic acquisitions, boosting sector performance. However, some companies, like Cochlear, have seen modest gains despite underwhelming profits, highlighting ongoing investor scrutiny of profitability versus expectations.

Sector performance during this reporting period reflects broader economic factors, including interest rate decisions, currency movements, and global commodity trends. Market analysts anticipate volatility as investors digest results, particularly around milestone levels for the S&P/ASX200. Overall, the reporting season is shaping up as a critical period for gauging corporate resilience, growth prospects, and investor sentiment across Australia’s equity market.

This week, Australia’s corporate earnings season showcased a mix of strong performances and cautious outlooks, influencing investor sentiment across the ASX.

Key Highlights:

Westpac reported a 14% rise in quarterly net profit to A$1.9 billion, surpassing expectations and driving a 6.3% surge in its share price. This performance bolstered the broader financial sector, despite Commonwealth Bank’s more modest results.

Telstra declared a 14% increase in adjusted operating earnings for FY25, totaling A$8.61 billion, and announced a A$1 billion share buyback. However, its earnings forecast for FY26 fell slightly below market expectations, leading to a 2% dip in its share price.

Cochlear delivered a 1% gain in its share price, despite reporting a A$392 million underlying net profit that underwhelmed investor expectations. Amcor experienced a significant 9.7% decline in its share price due to weaker-than-expected performance in its North American operations.

Baby Bunting shares soared 40.5% following strong earnings growth and expansion plans, highlighting resilience in the consumer sector.Overall, while the reporting season has delivered a mix of results, the ASX has reached record highs, fueled by robust earnings in key sectors and investor optimism.

That said, we expect the following trends to continue over the reporting period.

Earnings decline led by ASX200 Resources profits are forecast to fall 1.7% in FY25, marking the second consecutive year of contraction. The resources sector is the primary drag, with mining and energy earnings expected to drop nearly 20%, driven by weaker commodity prices and global demand.

Tech and Communication Services are likely to outperform In contrast, with technology and communication services as bright spots. Tech firms are projected to grow earnings by 30%, fuelled by digital transformation and AI adoption. Online classifieds and software providers are showing strong earnings momentum. Valuation risks remain a concern as the ASX trades at a forward P/E of 19.5–20x, well above historical averages. This raises the stakes for companies to meet or exceed expectations. Any earnings miss could trigger sharp market price reactions (refer to Figure 3 below).

Margin pressures and cost out are likely to remain a key theme. Companies are grappling with rising input costs, wage inflation, and interest rate uncertainty. Those with pricing power or operational efficiency are better positioned to defend margins.

Despite real wage growth and tax cuts, consumer confidence remains fragile due to high mortgage and rent costs. Retailers like Wesfarmers and JB Hi-Fi have outperformed, but sustainability is questioned. US tariffs and China’s sluggish recovery are impacting export-oriented sectors. While Australia is relatively insulated, firms with US exposure like Ansell and Breville face risks.

While FY25 may mark a low point, analysts expect earnings recovery in FY26, supported by potential rate cuts and improving global conditions.

Figure 3 – Australian Equity Market EPS Growth

Overview of the Australian Government Bond Market

Last week, the Australian bond market experienced notable activity, influenced by domestic economic developments and global market trends On August 12, the Reserve Bank of Australia (RBA) reduced the official cash rate by 25 basis points to 3.60%, marking the third rate cut of the year. This decision was driven by moderating inflation and a cooling labour market. Following the announcement, Australian government bond yields declined across the curve. The 10-year yield eased to 4.23%, down from 4.26% the previous day . Shorter-term yields also saw modest decreases, reflecting market expectations of continued accommodative monetary policy.

The Reserve Bank of Australia (RBA) reduced the official cash rate by 25 basis points to 3.60% on August 12, 2025—the third rate cut this year—citing several key factors:

Moderated Inflation: Underlying inflation has eased to 2.7% in the June quarter, aligning with the RBA’s 2–3% target range.

Slowing Economic Growth: Economic expansion has slowed, with GDP growth at 1.3% year-on-year and a 0.2% increase in the first quarter of 2025.

Rising Unemployment: The unemployment rate has increased to 4.3%, indicating a cooling labor market.

Global Economic Uncertainty: While global trade tensions persist, Australia has not yet shown significant negative impacts from these challenges. RBA Governor Michele Bullock emphasized that future rate decisions will depend on incoming economic data, with the possibility of further cuts if conditions warrant. This rate cut aims to stimulate economic activity while maintaining inflation within the target range. Economists anticipate that the RBA may implement additional rate cuts later in the year if economic conditions continue to support such measures. The Reserve Bank of Australia’s (RBA) August 2025 Statement on Monetary Policy provides a comprehensive assessment of the nation’s economic conditions and outlook.

Global Economic Conditions: The RBA anticipates a modest slowdown in global GDP growth during the latter half of 2025 and into 2026, influenced by higher tariffs and ongoing policy uncertainties. While U.S. growth is expected to decelerate, China’s economy is projected to remain resilient, supported by fiscal and monetary stimulus measures. The risks of a widespread trade war have diminished, but uncertainties persist regarding the effects of trade policies on global activity and inflation.

Domestic Economic Conditions: Domestically, the RBA has revised its GDP growth forecast for 2025 down to 1.7%, from the previous 2.1%, reflecting weaker-than-expected public demand and a lower outlook for productivity growth. The central bank attributes this productivity slowdown to factors such as weak wage growth, falling consumer spending, and reduced business profits. Consequently, the potential growth rate of the economy is now estimated at 2.0%, down from 2.25% previously.

Inflation and Monetary Policy: Inflation has moderated, with underlying inflation expected to remain around the midpoint of the RBA’s 2–3% target range. The cash rate was reduced to 3.6% in August 2025, marking the third rate cut of the year. The RBA indicated that further rate cuts may be considered if economic conditions warrant.

Labour Market: The unemployment rate is projected to remain stable at 4.3% over the forecast period. The labor market is expected to be close to full employment, though some tightness may persist. The RBA will continue to refine its assessment of full employment as more data becomes available.

Risks and Uncertainties: The RBA acknowledges heightened uncertainty regarding both domestic and global economic conditions. The central bank remains vigilant and ready to adjust monetary policy as necessary to achieve its objectives of price stability and full employment.

In summary, the RBA’s August 2025 Statement on Monetary Policy highlights a cautious economic outlook, with moderated inflation, slower economic growth, and ongoing uncertainties influencing monetary policy decisions.

In the corporate sector, the Commonwealth Bank of Australia (CBA) launched a $5 billion bond issuance, attracting over $8 billion in demand. The offering included both fixed and floating rate bonds with maturities of 3.25 and 5 years. The strong investor interest was attributed to a search for safe investment options amid market liquidity and strong equity valuations.

Looking ahead, the bond market remains attentive to upcoming economic data, particularly regarding inflation and employment figures. Analysts anticipate that the RBA may implement additional rate cuts later in the year if economic conditions continue to support such measures. The combination of lower rates and subdued inflation is expected to sustain investor interest in fixed-income securities.

In summary, the Australian bond market last week reflected a response to the RBA’s rate cut and strong corporate bond issuance, with yields adjusting accordingly and investor sentiment remaining cautiously optimistic.

Looking Ahead: Major Economic Releases for the Week Ending 15th August

| Date | Country | Release | Consensus | Prior |

|---|---|---|---|---|

| Tuesday, 19/08 | United States | Housing Starts Number | 1.295 | 1.321 |

| Wednesday, 20/08 | Australia | S&P Global Mfg PMI Flash | n/a | 51.3 |

| Wednesday, 20/08 | Australia | S&P Global Svs PMI Flash | n/a | n/a |

| Wednesday, 20/08 | Australia | S&P Global Comp PMI Flash | n/a | n/a |

| Thursday, 21/08 | United States | Initial Jobless Clm | 226 | 224 |

| Thursday, 21/08 | United States | Philly Fed Business Indx | 6 | 15.9 |

| Thursday, 21/08 | United States | S&P Global Mfg PMI Flash | 49.5 | 49.8 |

| Thursday, 21/08 | United States | S&P Global Svcs PMI Flash | 53.7 | n/a |

| Thursday, 21/08 | United States | S&P Global Comp PMI Flash | n/a | n/a |

| Thursday, 21/08 | United States | Existing Home Sales | 3.91 | 3.93 |

For more detailed weekly updates, YieldReport Weekly